58 Scientists Validated the Physics of a Fusion Power Plant. The $22 Billion Question Is Whether Anyone Can Build One.

Five peer-reviewed papers proved CFS’s ARC tokamak will work. Helion raised $465 million without publishing any. The fusion industry has collectively raised enough to build roughly three first-of-a-kind plants. It needs thirty.

On June 4, 2026, fusion energy split into two religions. Commonwealth Fusion Systems published five peer-reviewed papers in the Journal of Plasma Physics, co-authored by 58 physicists from MIT, Columbia, UC San Diego, KTH, Chalmers, and the Max Planck Institute, confirming that its ARC tokamak will produce 1.1 gigawatts of fusion power and deliver 400 megawatts of net electricity to the grid. On the same day, Helion Energy announced a $465 million raise at a $15.5 billion valuation—nearly tripling from $5.4 billion seventeen months earlier—without publishing a single peer-reviewed paper.

One company proved its reactor will work, and the other is worth four times as much. That is the entire fusion industry in miniature. The $30–50 billion question hanging over it is whether peer review or commercial velocity is a better predictor of who actually puts electrons on a wire, and right now the market is paying a 4× premium for the company that chose not to subject its physics to outside scrutiny.

The Publication Divergence

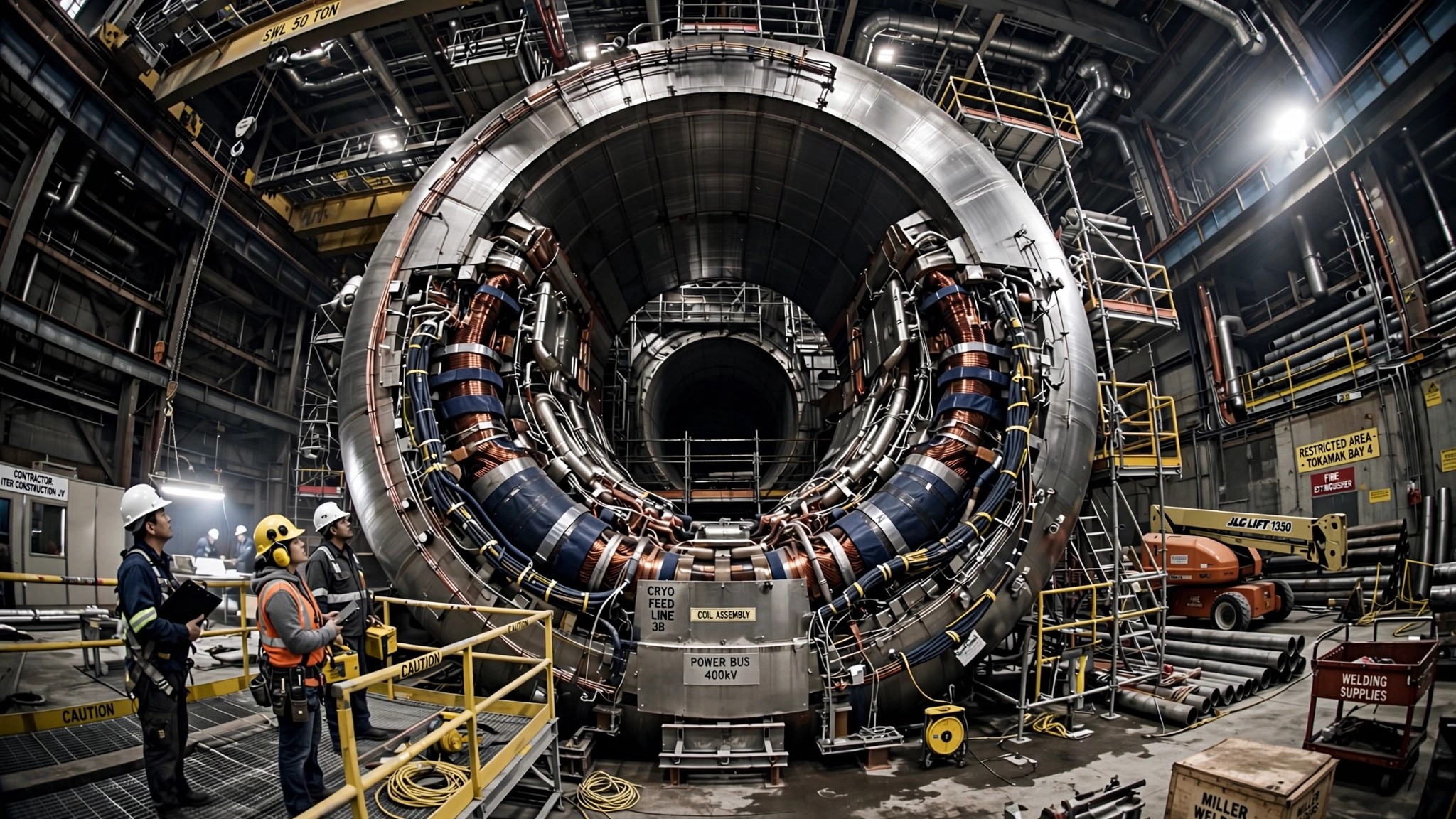

CFS has raised roughly $3 billion, completed a 20-tesla high-temperature superconducting magnet, and now has five independent papers validating ARC Version 3A: a 4.6-meter major radius tokamak producing 400 MW net, targeting Chesterfield County, Virginia, in the early 2030s. On April 28, CFS applied to PJM Interconnection—the first fusion company to formally request a slot on a major American grid. “If we build the ARC tokamak and power plant as we intend, it’ll work,” said chief engineer Alex Creely. That sentence contains the most important word in fusion: if.

Helion’s $15.5 billion buys a different story. The company has a Microsoft power purchase agreement (electricity by 2028), a Nucor deal for 500 MW of fusion-powered steelmaking, a Polaris machine that reached 150 million degrees with fusion fuel, and an Orion plant under construction in Malaga, Washington. Its Series G attracted Thrive Capital, Lux Capital, Peak XV Partners, and Bill Ford alongside Lightspeed, Mithril, SoftBank, and Dustin Moskovitz’s Good Ventures.

What it does not have—despite $1.5 billion in total funding, an Orion plant under construction, and a valuation that implies investors see a working power plant on the other side of it—is a single peer-reviewed physics paper.

TechCrunch flagged this directly: “Helion doesn’t frequently publish in peer-reviewed journals, so physicists haven’t been able to poke at the theoretical underpinnings.” CEO David Kirtley’s response deserves scrutiny rather than repetition: “We don’t want to theorize about fusion. We just want to go build it.” Fair enough. But CFS is also building—SPARC is 65 percent complete—and it published anyway. The question Kirtley’s dodge raises is not whether Helion prefers building to theorizing, but whether its field-reversed configuration physics can withstand external review. If magnets compressing fuel and harvesting electricity directly (no steam turbines) works as advertised, the engineering is radically simpler than a tokamak. If it doesn’t, $1.5 billion bought hardware and an unfalsifiable thesis. The market awarded a 4× valuation premium to the company that chose not to find out in public.

$2.5 Billion of New Money in a Single Week

CFS and Helion were not alone. Focused Energy ($240M), Thea Energy ($100M), and Inertia Energy ($450M from stealth) all closed rounds the same week, while General Fusion went public via a $1 billion SPAC—the first publicly traded pure-play fusion company, putting total private capital committed to fusion in 2026 alone above $3 billion. Sounds like a lot until you run the construction math.

The Math Nobody Is Running

CFS says its first ARC plant costs $2.5 billion for 400 MW: $6,250 per kilowatt. Compare:

| Technology | Cost per kW | Source |

|---|---|---|

| Utility-scale solar | $900–$1,200 | BNEF 2025 |

| Natural gas CC | $1,100–$1,400 | EIA AEO 2025 |

| Offshore wind | $3,000–$5,000 | IEA WEO 2025 |

| CFS ARC (estimate) | $6,250 | Company projection |

| Vogtle 3&4 (nuclear, actual) | $15,700 | Georgia PSC filings |

| ITER (research, actual) | $44,000 | ITER Organization |

Fusion at $6,250/kW undercuts Vogtle-era nuclear fission by 2.5 times, which sounds promising until you apply the only empirical overrun data for large-scale tokamak construction: ITER went from $5 billion to $22 billion, a factor of 4.4×. If CFS hits even half that (2.2×), ARC becomes $5.5 billion at $13,750/kW—Vogtle territory, with none of the regulatory track record and all of the first-of-a-kind risk. Nobody has built a commercial tokamak before. Nobody.

The funding arithmetic is worse. Total private fusion funding stands at $8–9 billion. CFS’s first plant alone eats $2.5 billion at face value. If every company currently operating builds one plant, the industry burns through its entire capital base without producing a commercial megawatt-hour, because first-of-a-kind plants consume capital for 4–7 years before generating revenue.

Where does the next $30–50 billion come from? Three options. Government (the DOE’s entire annual fusion budget is $1 billion), project finance (which requires cost certainty that doesn’t exist yet), or public markets where General Fusion is currently testing appetite for pre-revenue energy companies—pick one, because the math demands all three.

The Strongest Case for Fusion Anyway

ITER is a 35-nation government project whose cost overruns trace to multinational bureaucracy—procurement delays, specification changes cascading across seven partners, political allocations overriding engineering decisions—not physics. A private company with one site and one supply chain might genuinely build for $6,250/kW. SpaceX versus the Space Launch System is the analogy fusion advocates deploy, and it is not frivolous: organizational structure alone accounts for a 40× cost gap on comparable payloads.

The magnet case strengthens this. ITER’s low-temperature superconducting magnets require cooling to 4 Kelvin with liquid helium infrastructure that dominates the facility’s volume and cost. CFS’s REBCO tape magnets operate at 20 Kelvin, produce 20 tesla in physically smaller coils, and make a compact commercial tokamak possible rather than a cathedral-scale research installation. When 58 physicists confirmed the plasma physics works with these magnets, they eliminated the concern that HTS technology was oversold. What remains unproven is whether winding hundreds of tons of REBCO tape into production coils without defects can be done at the cost CFS projects. That question belongs to industrial engineering, not plasma physics, and the peer-reviewed papers do not answer it because it was not their job to ask.

What This Analysis Cannot Prove

The $2.5 billion estimate has not been independently reviewed and carries no contractual weight. ITER’s overrun ratio may be structurally inapplicable to a private single-site project, making the 2.2× sensitivity analysis either conservative or misleading. The $30–50 billion gap assumes multiple companies build simultaneously; consolidation around one or two winners would reduce the total substantially. Fusion cost projections have been wrong for six decades, and this analysis may simply add one more data point to that tradition.

What You Can Do

Investors: Distinguish companies with peer-reviewed validation from those without—CFS published; Helion has not—and note that General Fusion (GFUZ) and TAE are or will be publicly tradeable. The investable fusion thesis is five-plus years from revenue, and the strongest competing play is utilities building AI data center capacity now: Constellation Energy, NextEra, Dominion.

Policy: CFS’s PJM application is the first regulatory test of whether grid operators have a framework for fusion. The answer so far is that they don’t—fusion needs its own category, neither fission (which triggers NRC licensing) nor conventional generation.

Everyone else: Watch SPARC. CFS’s demonstration device targets net energy gain by 2027. If SPARC achieves Q>2, the ARC papers are validated experimentally, not just theoretically. If it misses, every timeline shifts. That is the single most important near-term data point in commercial fusion.

The Bottom Line

The physics of a commercial fusion power plant is now peer-reviewed and validated for at least one design. The construction question—whether a private company can build a novel plant for $2.5 billion when the only comparable project cost $22 billion—remains untested, unfunded at scale, and irreducible to a paper, no matter how many co-authors sign it. The fusion industry needs $30–50 billion more than it has, and the company most likely to deliver first is worth one-quarter the valuation of the competitor that refused to publish. We will know who was right by the time SPARC fires in 2027; by then, $22 billion in ITER lessons will have been paid for whether anyone learns from them or not.