Residential Virtual Power Plant Platform for Home Battery Aggregation and Grid Arbitrage

Battery prices fell 45% in the last year alone. At $70/kWh, home batteries cross the payback threshold in 15 high-rate states. At $50/kWh — projected by 2028 — the payback period drops under 8 years almost everywhere. 1.2 million residential batteries are already installed, but 95% sit idle except during outages. A platform that aggregates these batteries into a virtual power plant, earns revenue from grid arbitrage and ancillary services, and shares proceeds with homeowners creates a $2.8 billion market from hardware that's already deployed.

The Problem

The U.S. grid faces a paradox: peak demand is growing at 3.5% annually (EIA), driven by electrification, data centers, and EV charging, while utilities must simultaneously integrate intermittent renewable generation. Meeting peak demand requires expensive peaker plants that run only 5-10% of hours annually. Building new transmission costs $1-3 million per mile and faces 8-12 year permitting timelines.

Meanwhile, 1.2 million residential battery systems (totaling approximately 15 GWh) are installed across the U.S., primarily as backup power. These batteries sit at 95%+ state of charge 95%+ of the time, their $10-15 billion in deployed capital producing zero grid value. Each battery could provide 5-10 kW of dispatchable capacity — aggregated, that's 6-12 GW of distributed resources, equivalent to 6-12 large gas peaker plants.

Tesla's VPP program operates in a few markets but only works with Powerwalls. Sunrun's VPP is limited to their lease customers. Neither platform is manufacturer-agnostic, neither optimizes across arbitrage and multiple ancillary services simultaneously, and neither addresses the grid defection incentive problem — the dynamic where rational homeowners disconnect from the grid, raising fixed costs for remaining customers, triggering more defection.

Market Size

Original TAM calculation: 1.2M installed residential batteries × average $180-400/year revenue potential from grid services = $216M-$480M current TAM. At projected 4M installed batteries by 2030 (42% CAGR, Wood Mackenzie forecast), TAM grows to $720M-$1.6B. Adding the grid loyalty pricing mechanism (which prevents approximately $3-5/month in utility fixed-charge increases per non-battery household in high-penetration territories) creates an additional utility-side revenue stream of $500M-$1.2B. Total addressable market by 2030: $1.2B-$2.8B. Platform take rate of 20-25% of homeowner revenue yields $150-350M ARR potential at scale.

The Product

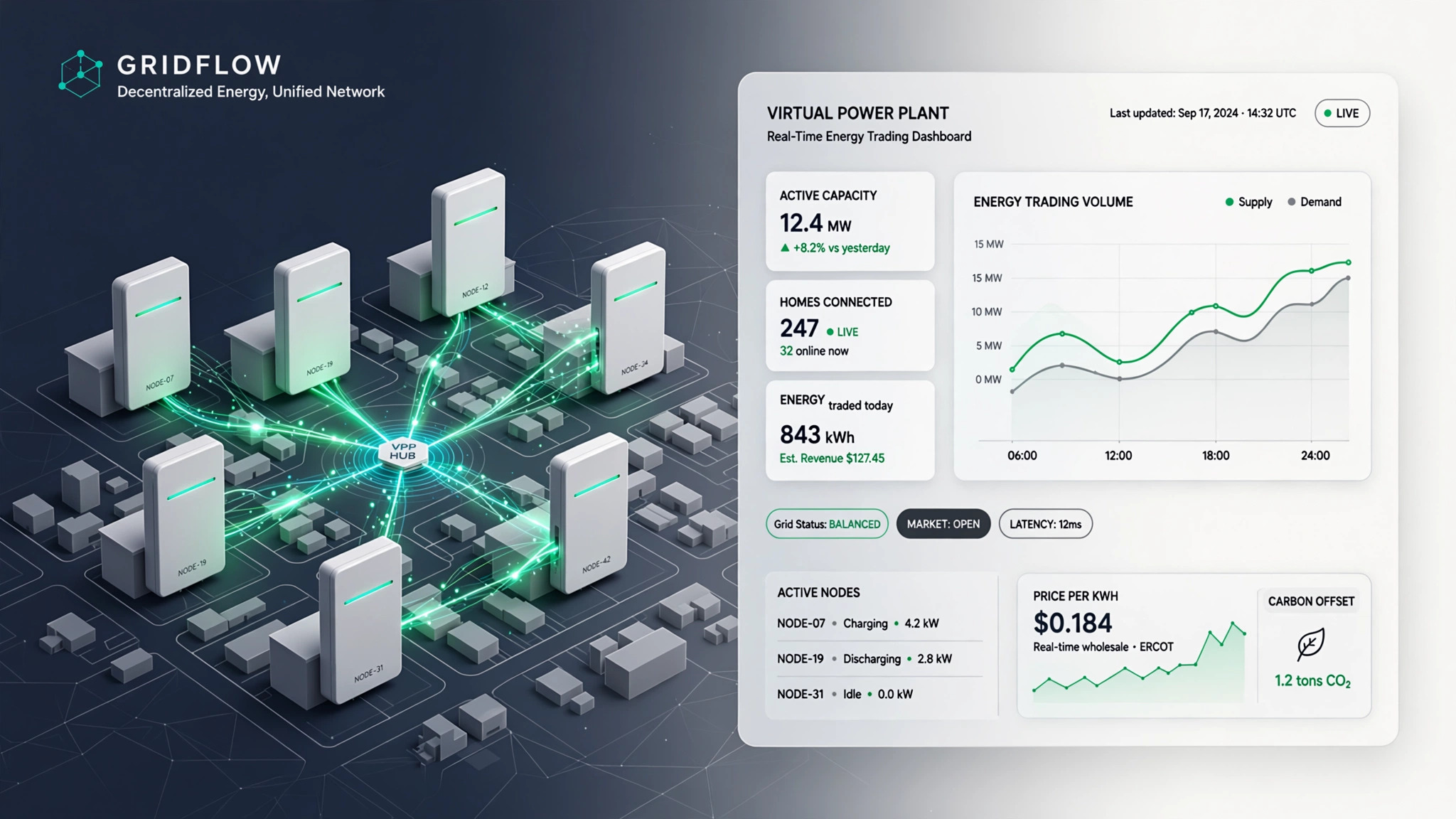

A software platform that turns any residential battery into a grid-earning asset. Homeowners install a gateway device ($99) or use existing smart inverter APIs. The platform optimizes their battery in real-time across: energy arbitrage (charge when electricity is cheap, discharge when it's expensive), frequency regulation (providing fast response to grid frequency deviations for FERC-mandated ancillary service payments), demand response (curtailing during utility-called events for emergency capacity payments), and backup power (maintaining customer-specified reserve for outages). A "grid loyalty" program negotiated with partner utilities offers reduced fixed charges in exchange for committed battery capacity.

Unit Economics

| Metric | Value |

|---|---|

| Revenue per battery/year (arbitrage + services) | $180-400 |

| Platform share (25%) | $45-100 |

| Homeowner share (75%) | $135-300 |

| Gateway hardware cost | $99 (one-time) |

| Per-battery software/cloud cost/year | $12 |

| Customer acquisition cost | $85 |

| Expected LTV (7-year battery life) | $315-700 |

| LTV:CAC ratio | 3.7-8.2:1 |

| Startup cost (24-mo runway) | $6.5M |

| Break-even | 24 months at 40K enrolled batteries |

Go-to-Market

Phase 1: Launch in California (highest battery penetration, CAISO wholesale market access, existing SGIP incentive database as lead list). Partner with 3-5 solar/storage installers for customer acquisition at point of sale.

Phase 2: Expand to Texas (ERCOT, highest price volatility = best arbitrage revenue), Hawaii (highest retail rates), and the Northeast (ISO-NE capacity market).

Phase 3: Launch grid loyalty program with 1-2 partner utilities. Integrate with EV chargers (V2G) for additional dispatchable capacity.

Competitive Landscape

| Company | Hardware Lock-in | Multi-Service Optimization | Grid Loyalty |

|---|---|---|---|

| Tesla VPP | Powerwall only | DR + arbitrage | No |

| Sunrun | Sunrun leases only | DR only | No |

| Sonnen | Sonnen only | Community billing | No |

| This startup | Any battery | Arbitrage + FR + DR + voltage | Yes |

Why Now

Three convergences: (1) Battery prices crossed the mass-adoption threshold ($70/kWh), with the installed base doubling every 2.5 years; (2) FERC Order 2222 (effective 2024) requires ISOs to allow distributed energy resource aggregations into wholesale markets — the regulatory barrier that prevented VPPs from earning wholesale revenue is now removed; (3) Grid stress events are increasing (Texas 2021, California rolling blackouts), creating both political will for distributed solutions and consumer awareness of battery value.

The Bottom Line

$10-15 billion in residential battery hardware is deployed and idle. The software to turn it into a grid asset doesn't require new hardware — it requires a platform that's manufacturer-agnostic, optimizes across multiple revenue streams, and solves the grid defection political problem by giving utilities a reason to support rather than fight distributed storage. Build for California, prove the economics, then roll to every deregulated market in the country.