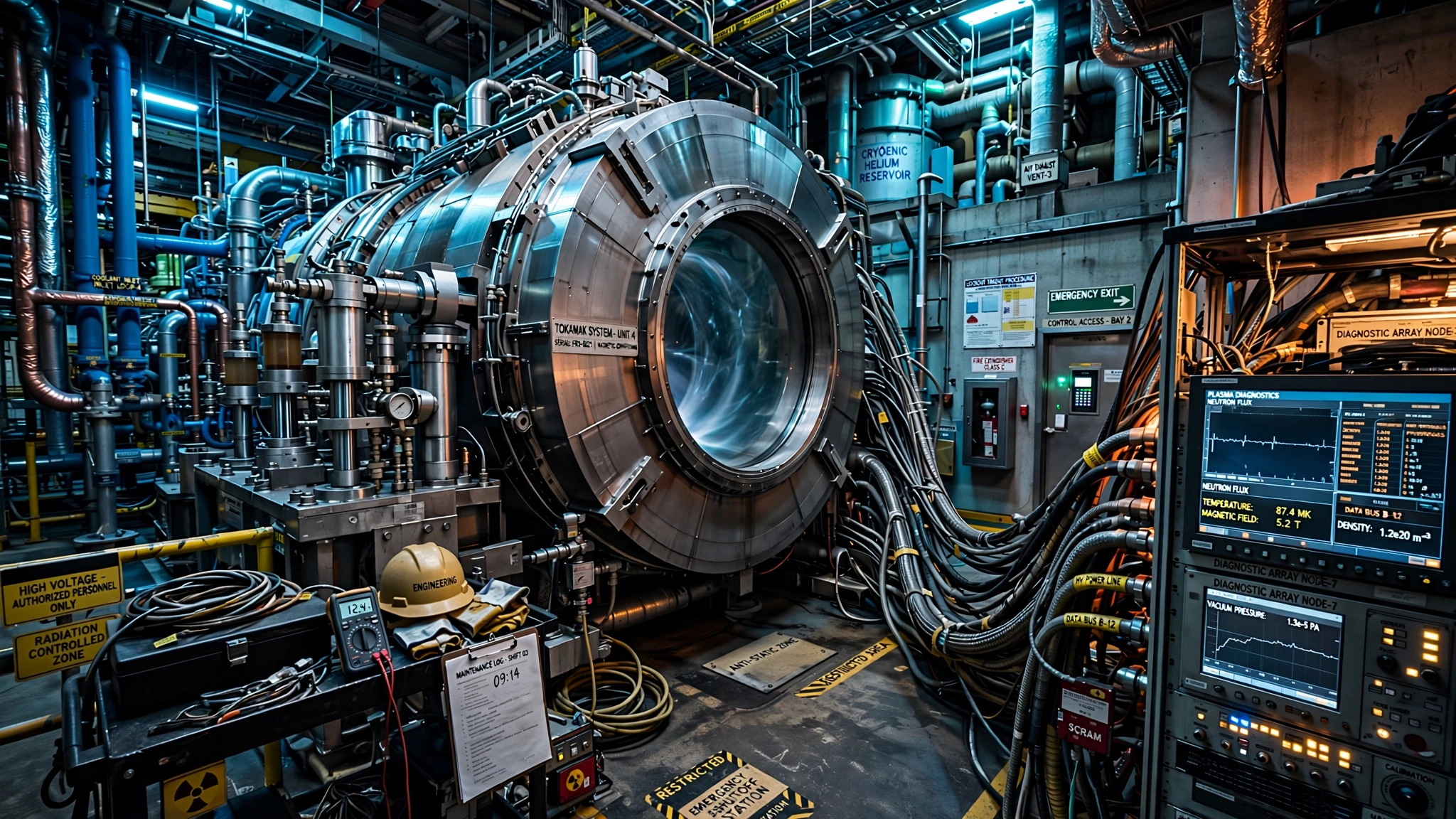

On June 22, General Fusion announced that its Lawson Machine 26, a cylindrical device roughly the size of a small bus that uses industrial pistons to mechanically compress magnetized plasma inside a spinning vortex of liquid lithium, heated that plasma to 8.4 million degrees Celsius by squeezing it. In the language of plasma physics, that translates to 0.72 keV, and the company needs to reach roughly 10 keV for its magnetized target fusion approach to produce the conditions required for commercial energy generation, which means the headline result represents 7.2% of the temperature target on a linear scale. On a fusion-power scale, where reaction rates grow roughly with the square of temperature, General Fusion has covered about 0.5% of the distance to commercially relevant conditions.

Four days before that announcement, the SEC declared effective the registration statement for General Fusion's merger with Spring Valley Acquisition Corp. III, a blank-check company whose previous nuclear SPAC, NuScale Power, has since lost more than half its market value from its all-time peak. The deal values the combined entity at approximately $1 billion in pro-forma equity, with a $600 million pre-money valuation, zero revenue, zero commercial reactors, and zero demonstrated net energy gain, while the company expects to build its first power plant sometime in the mid-2030s.

Divide the $635 million in total post-merger capitalization by 0.72 keV and you get $882 million per keV of demonstrated capability, a metric nobody in the fusion industry uses, which is precisely why it reveals something the conventional narrative misses.

A Calculation Nobody Ran

General Fusion has spent roughly two decades and an estimated $300 million in private capital to arrive at a plasma temperature of 0.72 keV, and the SPAC transaction adds approximately $335 million more through a combination of $108 million from an oversubscribed private investment in public equity and about $230 million from SVAC III's cash held in trust, assuming no share redemptions at closing, which brings total capitalization after the merger to around $635 million for a company that has built exactly one demonstration machine, never produced net energy, laid off 25% of its workforce in 2025, and recently pushed its scientific breakeven target from 2026 to 2028.

For that money, General Fusion has accomplished things that deserve genuine respect: constructing a commercially relevant-scale MTF demonstration machine, compressing plasma with a lithium liner and tripling electron temperature through mechanical compression alone, observing neutron yield increases that signal fusion reactions occurring inside the chamber, and securing partnerships with the UK Atomic Energy Authority, Princeton Plasma Physics Laboratory, and General Atomics for diagnostic support and validation. These are not trivial achievements, and they represent the only data points in human history confirming that magnetized target fusion works at this scale.

But the remaining milestones stretch far ahead, and they get harder as the numbers climb. One keV comes next, a 39% improvement over the current record that the company hopes to reach within LM26's operating envelope, followed by the 10 keV threshold and ultimately the full Lawson criterion, which demands not just temperature but the simultaneous achievement of sufficient plasma density and energy confinement time in a triple-product trifecta that no private fusion company has ever demonstrated. Here is what the cost-per-keV comparison reveals across the competitive landscape:

| Company | Approach | Total Capital | Temperature Milestone | Cost/keV |

|---|---|---|---|---|

| General Fusion | Magnetized Target (MTF) | ~$635M (incl. SPAC) | 0.72 keV (achieved) | $882M/keV |

| CFS | Compact Tokamak (HTS) | ~$3B | Target: 8.6+ keV (SPARC) | $349M/keV (target) |

| Helion | Field-Reversed Config | ~$1.6B | ~13 keV (compressed) | $123M/keV (claimed) |

| TAE Technologies | Aneutronic FRC (p-B11) | ~$2B | ~0.9 keV (Copernicus) | ~$2.2B/keV |

| ITER | Tokamak | $25B+ | Target: ~10 keV | $2.5B/keV (target) |

Three patterns emerge from this data, and each tells a different story about the fusion industry's relationship with capital. Helion claims the lowest cost-per-keV by a wide margin, although its compressed-plasma temperature measurements involve microsecond pulses that critics argue are not directly comparable to approaches that sustain plasma for longer durations inside magnetic or mechanical confinement structures. General Fusion sits in the middle of the pack, a position that is actually less damning than it appears for a company that deliberately avoided the superconducting magnets costing hundreds of millions that CFS requires and the laser systems filling entire buildings that NIF depends upon. And every company in the table, without exception, has burned through its entire capital allocation without demonstrating net energy gain, which means every dollar invested so far represents a bet on physics that remains unproven in any privately financed reactor on Earth.

What the Numbers Mean for GFUZ Investors

At the current cost rate of $882 million per keV achieved, closing the remaining gap from 0.72 keV to 10 keV would require an additional $8.2 billion in capital, a sum that exceeds by a factor of 13 the total proceeds available from the entire SPAC transaction and that approaches triple what Commonwealth Fusion Systems, the best-funded private fusion company, has raised across all rounds since its MIT spinout in 2018. That math is deliberately aggressive because it assumes linear cost scaling, and engineering does not actually work that way: early milestones consume disproportionate capital since you are simultaneously designing the machine from scratch, assembling a team of plasma physicists willing to work for a startup rather than a national lab, building diagnostic infrastructure that did not previously exist for your reactor topology, and proving fundamental physics concepts that nobody has attempted at commercially relevant scale before.

But fusion possesses a deeply counterintuitive property that bends the cost curve back in the wrong direction at higher parameters. Plasma instabilities grow more violent as temperature and pressure rise, energy losses from radiation and particle escape follow nonlinear scaling laws that punish incremental progress disproportionately, and the structural materials surrounding the reaction chamber face 14.1 MeV neutron bombardment that degrades them over timescales much shorter than commercial reactor lifetimes demand. ITER was budgeted at $5 billion in 2006 and has since blown past $25 billion with the reactor still years from first plasma, a cost trajectory that makes the linear $8.2 billion extrapolation for General Fusion look almost gentle by comparison.

Spring Valley itself is a cautionary case study that GFUZ investors should examine closely. Its first SPAC vehicle merged with NuScale Power, a small modular fission reactor company that, unlike General Fusion, actually holds NRC design certification for a real reactor type and has progressed further toward commercial deployment than any private fusion company. NuScale's stock still fell more than 50% from its peak, because quarterly earnings cadences demand progress narratives that complex nuclear engineering does not always deliver on Wall Street's preferred schedule.

Real Physics, Real Results

None of the financial skepticism above should obscure what actually happened in that Vancouver laboratory on June 22, because the LM26 results are genuine science confirmed by multiple independent diagnostic systems and significant enough that the company submitted the technical paper for peer review while simultaneously making it publicly available, a transparency combination that is rare in a sector where many competitors guard their data behind non-disclosure agreements and investor decks that nobody outside the boardroom ever sees. Electron temperature rose to 0.72 keV with an uncertainty band of plus or minus 0.08 keV, plasma density along with poloidal magnetic field both increased roughly tenfold during compression in results that match or exceed what General Fusion's smaller test beds produced but at dramatically larger scale, and the plasma remained stable deep into the compression phase without the catastrophic disruptions that theorists had warned might render liner-driven fusion physically impossible.

Most critically for the company's long-term viability, there was no significant contamination of the plasma by the lithium liner during the stable compression phase. This single observation may matter more than the temperature headline, because lithium contamination had been the most persistent theoretical objection to magnetized target fusion since General Fusion's founding in 2002: if liquid lithium atoms infiltrate the plasma during compression, they radiate energy away through atomic line emission and cool the plasma faster than mechanical work can heat it, creating a thermodynamic death spiral that no amount of engineering optimization or additional capital can overcome. The fact that contamination did not occur removes what many plasma physicists had long considered the most likely fundamental failure mode for the entire MTF concept.

Results also matched the company's computational models across every major diagnostic, which matters enormously for predicting what happens at parameters the machine has not yet reached, and the agreement between simulation and experiment is the specific technical detail that should give investors the most confidence, because when your computational predictions match your physical measurements, you have a tool for exploring the future without paying the full cost of running every experiment.

An Unforgiving Competitive Landscape

General Fusion enters the public markets at a moment when its better-funded competitors are accelerating in ways that make the $1 billion SPAC valuation look modest, and perhaps appropriately so. Helion Energy closed a $465 million Series G in June 2026 at a $15.5 billion valuation, making it the most valuable private fusion company on Earth with roughly 15 times General Fusion's post-merger market capitalization, and it is simultaneously building both a prototype called Polaris and a commercial reactor called Orion in Washington State while holding a power purchase agreement with Microsoft for 50 megawatts of electricity, a deal backed in part by Sam Altman's approximately one-third ownership stake in the company.

Commonwealth Fusion Systems has raised close to $3 billion and is in the process of assembling SPARC, a compact tokamak that uses high-temperature superconducting magnets producing fields roughly twice as strong as conventional superconductors, enabling a reactor under five meters in diameter to theoretically match the output of ITER's 16.4-meter behemoth at a fraction of the cost. CFS published five peer-reviewed papers in June 2026 validating the physics of its approach and has begun selling superconducting magnets commercially, generating actual revenue while its reactor progresses through assembly.

TAE Technologies chose yet another path to public markets, merging with Trump Media & Technology Group at a combined valuation exceeding $6 billion, and unlike General Fusion, TAE generates real revenue from power electronics and radiation therapy for cancer treatment, giving public shareholders something concrete to discuss on quarterly calls beyond the latest plasma temperature reading.

General Fusion's thesis against this backdrop is straightforward: mechanical compression will be cheaper to commercialize than any of these alternatives because it replaces superconducting magnets, exotic materials, and petawatt lasers with industrial pistons and replaceable liquid lithium walls. The thesis is intellectually coherent and physically plausible and entirely untested at commercial scale.

What This Analysis Did Not Prove

The cost-per-keV framework carries genuine limitations that should not be glossed over in the service of a clean narrative. Different fusion approaches target fundamentally different operating regimes with distinct plasma configurations, confinement mechanisms, and pulse durations, which means that comparing peak electron temperatures across companies is inherently imprecise in ways that no single financial metric can fully capture. Helion achieves its keV numbers in microsecond bursts during violent plasma collisions, CFS aims to sustain lower temperatures for much longer durations inside a magnetic bottle, and General Fusion compresses plasma mechanically in a process that resembles a diesel engine's compression stroke more than it resembles either competitor's approach.

Temperature is also only one of three variables in the Lawson criterion. General Fusion's 10x increase in plasma density during compression may actually constitute the more significant result than the temperature headline, because the MTF approach is specifically designed to drive temperature, density, and confinement time simultaneously through a single mechanical stroke rather than optimizing each parameter independently. A cost-per-keV metric systematically undervalues approaches that use compression to boost all three variables at once.

I also lack audited pre-SPAC financials for General Fusion, and the breakeven target slippage from 2026 to 2028 could reflect genuinely disappointing technical results, a strategic decision to present more credible timelines ahead of a public listing, or both simultaneously, with only the company's internal team knowing the true explanation.

Steel-Manning General Fusion

The cost-per-keV framework may fundamentally misread what magnetized target fusion offers, because General Fusion's core argument has never been that it will reach fusion conditions first or cheapest in the laboratory. Its argument, and the one that undergirds the entire $600 million pre-money valuation, is that when it eventually reaches those conditions, the reactor architecture surrounding them will be so dramatically cheaper to construct, operate, maintain, and replicate than any tokamak, any laser facility, and any field-reversed configuration that the capital disadvantage it faces today becomes irrelevant at the commercialization stage.

Consider what LM26 conspicuously does not require. No superconducting magnets, each costing tens of millions of dollars while demanding liquid helium cooling infrastructure that constitutes its own multi-million-dollar engineering challenge. No petawatt laser arrays occupying entire buildings and consuming enough electricity to power small cities during each shot. No exotic first-wall materials engineered to withstand decades of 14.1 MeV neutron bombardment, because the liquid lithium itself serves as the first wall and can be continuously replenished through a pumping system built from technology that the metallurgical industry has used for generations. The pistons that provide compression are standard precision hydraulic components available from industrial suppliers worldwide, and the lithium is a commercially traded commodity.

If the physics validates through peer review and continued experimentation at higher parameters, General Fusion argues, you could build commercial MTF reactors in existing heavy-industrial facilities, service them with mechanical and electrical engineers rather than requiring a staff of specialized plasma physicists, and replicate them at production rates that resemble manufacturing more than megaproject construction. The $600 million pre-money valuation, viewed this way, is not pricing 0.72 keV of temperature achievement. It is pricing the discovery that mechanical compression produces clean, stable, contamination-free plasma heating at commercially relevant scale, a discovery that, if it survives replication, transforms the entire cost structure of the path from laboratory fusion to grid-connected power generation.

What You Can Do With This

If you are considering GFUZ shares after the merger closes, anchor your expectations to three concrete data points before deciding your position size: the company has reached 7.2% of its temperature target after two full decades of operation, its scientific breakeven timeline has already slipped by two years in the five months between the SPAC announcement and the updated investor presentation, and the SPAC sponsor's only prior nuclear merger has underperformed its peak by more than half. This is a binary bet on whether specific physics will work at specific parameters within a specific timeframe, not a conventional growth equity trade with revenue multiples and comparable transactions, and the position should be sized for the realistic possibility that the answer turns out to be no.

If you follow energy policy, recognize that General Fusion's and TAE Technologies' public listings are creating the first sustained public-market accountability for fusion companies, forcing quarterly SEC disclosures of technical progress in formats that privately held competitors like Helion and CFS can avoid entirely. This transparency benefits a field that has historically operated on trust, optimistic timelines, and investor presentations that nobody outside the cap table independently verifies, though it carries real risk: if GFUZ underperforms in its first year as a public company, retail investors and congressional appropriators may conclude that fusion itself is the problem rather than recognizing that one particular company's approach encountered difficulty.

If you track the science itself, watch the peer review of the LM26 results with particular attention to the contamination findings. Independent confirmation that mechanical compression produced stable, contamination-free plasma heating with measurable neutron yield would formally establish MTF as a third credible pathway to fusion energy alongside magnetic confinement and inertial confinement. Three viable paths to the same destination represent significantly better odds than two, and the validation of any new confinement approach, regardless of which company achieves it, makes the broader quest for fusion energy meaningfully more likely to succeed within a timeline that matters for climate policy.

Bottom Line

General Fusion built a machine that heats plasma by squeezing it with industrial pistons and liquid lithium, and that machine works well enough to triple electron temperature to 0.72 keV, produce fusion neutrons, maintain plasma purity through the compression cycle, and match computational predictions across every major diagnostic measurement. At $882 million per keV of demonstrated progress, the $1 billion SPAC, a price that places General Fusion squarely in the middle of the fusion industry's capital efficiency curve: more cost-effective per unit of physics progress than ITER's $25 billion tokamak or TAE's $2 billion field-reversed configuration, but far behind the claimed efficiency of Helion's $15.5 billion rocketship or the targeted efficiency of CFS's $3 billion compact reactor. Whether $882 million per keV turns out to be a bargain depends entirely on what happens between 0.72 keV and 10 keV, a gap that consumed 20 years and $300 million to begin closing. Markets are betting that the rest of the journey will cost less per unit of progress than the beginning. The history of fusion engineering, measured in ITER's cost overruns and NuScale's stock chart and the graveyard of startups that preceded this generation, says it will cost more.