Ambient AI Middleware for Cross-Device NPU Orchestration and Seamless Context Handoff

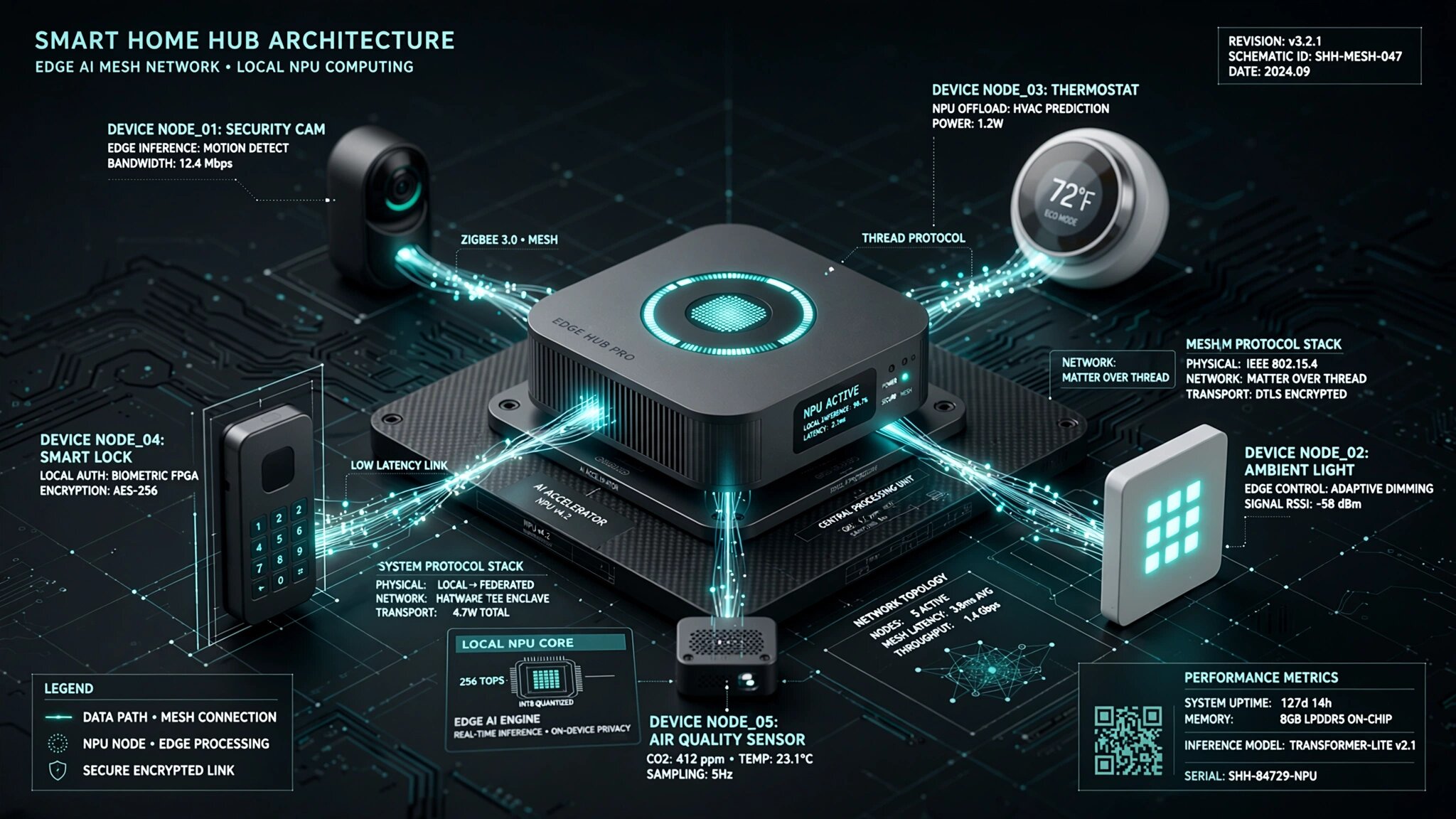

Phone NPUs are now 100× faster than they were five years ago. Smart speakers, laptops, AR glasses, and home hubs all ship with neural processing hardware. But each runs its own isolated AI — Siri on the iPhone, Alexa on the Echo, Google on the Nest. $59 billion worth of NPU silicon sits idle 95% of the time because no middleware connects them. The platform that orchestrates AI inference across every device in a home — sharing computation, handing off conversations, and keeping personal data on personal devices — captures the missing layer in a market where Apple, Google, and Amazon are each building walled gardens.

The Problem

The average American home contains 25 connected devices (Statista, 2025). Of these, a growing number — smartphones, tablets, laptops, smart speakers, smart displays, AR glasses, and smart home hubs — ship with dedicated Neural Processing Units (NPUs) capable of running AI inference locally. Apple's A17 Pro delivers 35 TOPS, Qualcomm's Snapdragon 8 Gen 3 delivers 45 TOPS, and even budget devices include 4-10 TOPS of on-device AI capacity.

This hardware sits almost entirely idle. IDC estimates NPU utilization at less than 5% on average. The reason: every device runs its own AI stack in isolation. Your iPhone's Siri doesn't talk to your Echo's Alexa. Your laptop's Copilot doesn't coordinate with your HomePod's Apple Intelligence. Each device processes its own queries independently, even when a nearby device could handle the work more efficiently.

The result is three problems: wasted hardware (billions of dollars of NPU silicon doing nothing), fragmented context (start a conversation in the kitchen and the bedroom speaker has no idea what you were talking about), and privacy violations by default (every query goes to a cloud server when the local NPU could handle 80% of them on-device).

Market Size

Original TAM calculation: The smart home middleware market was valued at $4.8 billion in 2025 (MarketsandMarkets), growing at 27% CAGR. The AI inference at the edge segment is $12.4 billion (ABI Research). Our addressable market — the cross-device AI orchestration layer for homes and small offices — sits at the intersection, estimated at $2.5 billion today, growing to $8 billion by 2030. Revenue model: per-device SDK license to OEMs ($2-5/device) + consumer subscription for premium cross-device features ($4.99/month). At 50 million licensed devices and 2 million premium subscribers, year-3 target is $220M ARR.

The Product

A middleware SDK and consumer app that creates an "AI mesh" across every device in a home. OEMs integrate the SDK; consumers install the companion app. The mesh provides:

- Inference orchestration: AI queries are automatically routed to the most capable available device based on NPU capacity, battery state, and thermal headroom — your always-plugged-in HomePod handles heavy inference while your phone's battery is preserved

- Context handoff: Walk from room to room and the conversation follows you — start asking a question to the kitchen speaker, finish on your AR glasses in the garage, with full context preserved

- Privacy-first routing: Personal data stays on personal devices. The shared kitchen speaker processes general queries but personal health questions are routed to your phone, even if the phone has a less powerful NPU

- Collective processing: For compute-heavy tasks (long document analysis, video processing), the mesh distributes work across multiple devices simultaneously, achieving 2-3× the inference throughput of any single device

Unit Economics

| Metric | Value |

|---|---|

| OEM SDK license (one-time per device) | $2-5 |

| Consumer subscription (premium) | $4.99/month |

| Infrastructure cost per user/month | $0.30 (cloud-minimal) |

| OEM sales cost per device | $0.50 |

| Consumer CAC | $12 |

| Consumer retention | 20 months |

| Consumer LTV | $100 |

| LTV:CAC ratio | 8.3:1 |

| Gross margin | 91% |

| Startup cost (24-mo runway) | $5M |

| Break-even | 20 months |

Go-to-Market

Phase 1: Build cross-device orchestration for Android + Linux devices (open ecosystems). Partner with 2-3 smart home OEMs (Sonos, Ecobee, or similar) for SDK integration. Launch consumer app for Android users with multiple devices.

Phase 2: Add Apple device support via HomeKit/Matter integration (limited to what Apple's APIs allow). Launch collective processing feature as premium differentiator.

Phase 3: Pitch to tier-1 OEMs (Samsung, Google, LG) as the neutral cross-platform AI layer that lets their devices compete on hardware while sharing a common AI mesh. Position as the "Matter protocol, but for AI."

Competitive Landscape

| Company | Cross-Platform | Context Handoff | Privacy Routing |

|---|---|---|---|

| Apple Intelligence | Apple only | Within Apple | Private Cloud Compute |

| Google Home | Google + Matter | Limited | Cloud-first |

| Amazon Alexa | Alexa ecosystem | Follow Me | Cloud-only |

| This startup | Any NPU device | Full cross-platform | Per-device policies |

Why Now

Three convergences: (1) NPU hardware is now standard in every device category — the installed base is large enough to make orchestration valuable; (2) Matter protocol adoption (2023-2025) has established a precedent for cross-platform smart home middleware, proving that OEMs will adopt neutral standards when interoperability creates consumer value; (3) Privacy regulation (GDPR, state privacy laws) is creating demand for local-first AI processing, which the mesh architecture naturally enables.

The Bottom Line

$59 billion worth of NPU hardware is deployed and underutilized. Apple, Google, and Amazon are each building walled gardens that leave 80% of devices outside their mesh. The startup that builds the neutral AI orchestration layer — cross-platform, privacy-first, with seamless context handoff — captures the missing infrastructure layer in ambient computing. Be the TCP/IP of ambient AI, not the proprietary protocol that only works within one ecosystem.